FD vs Mutual Fund: When it comes to safe and smart investing in India, two popular options always come up — Fixed Deposits (FDs) and Mutual Funds. Many investors, especially beginners, get confused about where to invest their money for better returns and safety.

Both investment options have their own advantages and risks. While Bank Fixed Deposits are known for stability and guaranteed returns, Mutual Funds offer higher growth potential through market-linked investments.

In this article, we will compare FD vs Mutual Fund based on returns, risk, liquidity, taxation, and investment goals to help you make the right financial decision in 2026.

Table of Contents

- What is a Fixed Deposit (FD)?

- What is a Mutual Fund?

- FD vs Mutual Fund: Key Differences

- Who Should Invest in Fixed Deposits?

- Who Should Invest in Mutual Funds?

- FD vs Mutual Fund: Which is Better for Beginners?

- Example: FD vs Mutual Fund Investment

- Final Verdict: FD or Mutual Fund?

- FAQs

What is a Fixed Deposit (FD)?

A Fixed Deposit is a financial product offered by banks and financial institutions where you deposit a lump sum amount for a fixed period at a predetermined interest rate.

The interest rate remains fixed throughout the tenure, making FDs one of the safest investment options in India.

Features of Fixed Deposits

- Guaranteed returns

- Fixed interest rate

- Low risk investment

- Flexible tenure from 7 days to 10 years

- Suitable for conservative investors

Average FD Returns in 2026

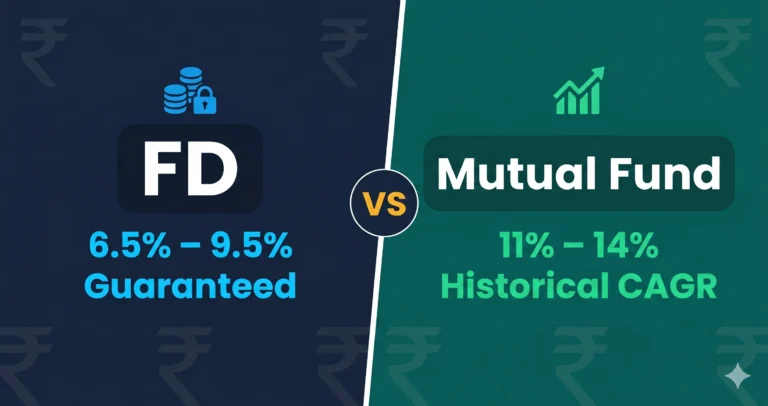

Most Indian banks currently offer FD interest rates between 6% and 8% annually depending on tenure and customer category. Senior citizens usually get slightly higher interest rates.

What is a Mutual Fund?

A Mutual Fund pools money from multiple investors and invests it in stocks, bonds, or other securities. Professional fund managers manage these investments to generate returns.

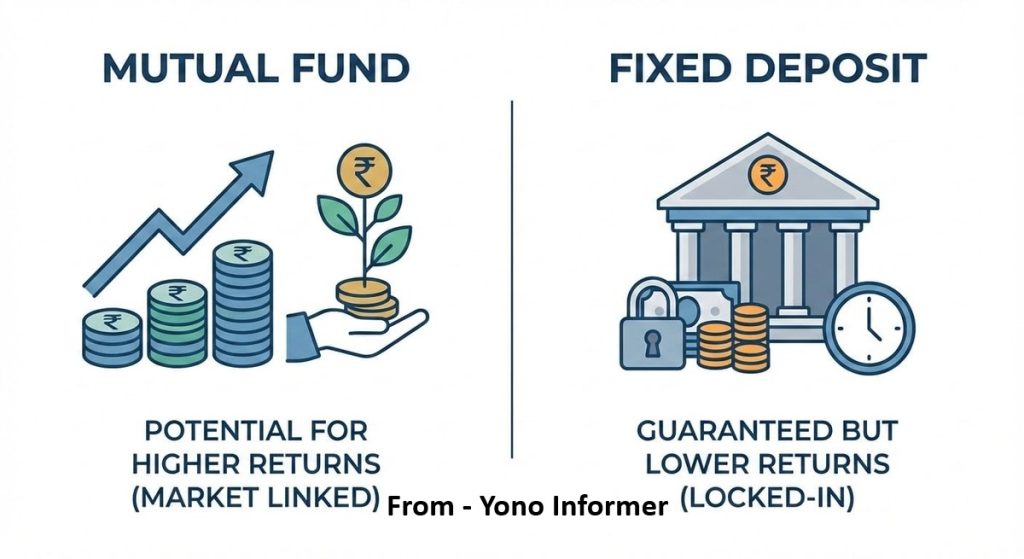

Unlike FDs, mutual fund returns are market-linked and not guaranteed.

Types of Mutual Funds

- Equity Mutual Funds

- Debt Mutual Funds

- Hybrid Funds

- Index Funds

- SIP Investments

Features of Mutual Funds

- Potential for higher returns

- Market-linked growth

- Professionally managed

- Diversified portfolio

- Suitable for long-term wealth creation

FD vs Mutual Fund: Key Differences

1. Returns Comparison

Fixed Deposits

FDs provide fixed and predictable returns. You know exactly how much money you will receive at maturity.

Example:

If you invest ₹1 lakh at 7% interest for 5 years, your maturity amount will be around ₹1.40 lakh.

Mutual Funds

Mutual fund returns depend on market performance. Equity mutual funds have historically delivered 10% to 15% annual returns over the long term.

Example:

A ₹1 lakh investment in a good equity mutual fund may grow to ₹1.60 lakh or more in 5 years depending on market conditions.

Winner:

Mutual Funds generally provide higher returns than FDs over the long term.

2. Risk Factor

Fixed Deposits

FDs are considered very safe because returns are guaranteed by banks. There is minimal risk unless the financial institution faces serious financial issues.

Mutual Funds

Mutual funds carry market risk. Returns can fluctuate based on stock market performance. Short-term losses are possible, especially in equity funds.

Winner:

FDs are safer for risk-averse investors.

3. Liquidity

Fixed Deposits

You can withdraw FD money before maturity, but banks usually charge a penalty.

Mutual Funds

Most open-ended mutual funds allow easy withdrawal anytime. Money is usually credited within 1–3 working days.

Winner:

Mutual Funds offer better liquidity.

4. Taxation

FD Taxation

Interest earned from FDs is fully taxable according to your income tax slab. Banks also deduct TDS if interest exceeds the prescribed limit.

Mutual Fund Taxation

Mutual funds enjoy comparatively better tax treatment.

- Equity funds held over 1 year qualify for long-term capital gains tax.

- Debt funds are taxed differently based on holding period and applicable rules.

Winner:

Mutual Funds are generally more tax-efficient.

5. Inflation Impact

Fixed Deposits

FD returns sometimes fail to beat inflation. If inflation is 6% and your FD gives 6.5%, your real returns are very low.

Mutual Funds

Equity mutual funds have historically beaten inflation over long periods.

Winner:

Mutual Funds perform better against inflation.

Who Should Invest in Fixed Deposits?

FDs are ideal for:

- Senior citizens

- Conservative investors

- People looking for guaranteed returns

- Investors with short-term financial goals

- Emergency fund parking

If safety is your highest priority, fixed deposits are a good option.

Who Should Invest in Mutual Funds?

Mutual funds are suitable for:

- Young investors

- Long-term wealth creators

- Investors comfortable with moderate risk

- People planning retirement

- Investors seeking higher returns

SIP (Systematic Investment Plan) is one of the best ways to invest in mutual funds regularly.

FD vs Mutual Fund: Which is Better for Beginners?

For beginners, the right choice depends on financial goals and risk tolerance.

Choose FDs if:

- You want stable income

- You cannot tolerate market fluctuations

- You need guaranteed returns

Choose Mutual Funds if:

- You want long-term wealth growth

- You can stay invested for 5+ years

- You are comfortable with market risk

A balanced approach is often the best strategy. Many financial experts recommend keeping some money in FDs for safety and investing the remaining amount in mutual funds for growth.

Example: FD vs Mutual Fund Investment

Suppose you invest ₹5 lakh for 10 years.

In Fixed Deposit

At 7% annual return: Your investment may grow to approximately ₹9.83 lakh.

In Equity Mutual Fund

At 12% average annual return: Your investment may grow to around ₹15.5 lakh.

This example shows the power of compounding in mutual funds over the long term.

Advantages of Fixed Deposits

- Guaranteed returns

- Safe investment option

- No market volatility

- Easy to understand

- Suitable for retirees

Disadvantages of Fixed Deposits

- Lower returns

- Taxable interest income

- Inflation may reduce real returns

- Premature withdrawal penalty

Advantages of Mutual Funds

- Higher return potential

- Professional fund management

- Diversification

- SIP investment flexibility

- Better inflation protection

Disadvantages of Mutual Funds

- Market risk

- Returns are not guaranteed

- Requires long-term patience

- Short-term volatility

Final Verdict: FD vs Mutual Fund?

There is no single “best” investment for everyone.

- If your priority is safety and guaranteed returns, Fixed Deposits are a better option.

- If your goal is long-term wealth creation and beating inflation, Mutual Funds are usually the smarter choice.

In 2026, many smart investors are using both FDs and Mutual Funds together to balance safety and growth. The ideal investment strategy depends on your age, financial goals, income, and risk appetite.

Frequently Asked Questions (FAQs)

Fixed Deposits are safer because they offer guaranteed returns and are not affected by market fluctuations.

Yes, equity mutual funds have historically provided higher long-term returns compared to FDs.

SIP in mutual funds can generate better long-term wealth, while FDs provide stable and fixed returns.

Yes, mutual funds carry market risk. However, long-term investments in quality funds can reduce risk significantly.

Senior citizens usually prefer FDs because of stable returns and lower risk.

Yes, market fluctuations can cause temporary losses, especially in equity mutual funds.