How to Improve Credit Score: 10 Effective Tips to Increase Your CIBIL Score – Our credit score plays a major role in your financial life. Whether you want to apply for a personal loan, home loan, credit card, or even rent a house, lenders and financial institutions often check your credit score before approving your application. A good credit score not only increases your chances of approval but also helps you get lower interest rates and better financial offers.

In India, credit scores usually range between 300 and 900. A score above 750 is generally considered excellent. If your score is low, don’t worry. Improving your credit score is possible with the right financial habits and discipline.

In this article, we will discuss 10 effective ways to improve your credit score quickly and maintain a healthy financial profile.

Table of Contents

- Pay Your Bills on Time

- Keep Your Credit Utilization Low

- Check Your Credit Report Regularly

- Avoid Applying for Multiple Loans Together

- Maintain Old Credit Accounts

- Diversify Your Credit Mix

- Clear Outstanding Debts Quickly

- Avoid Settling Loans Improperly

- Use Credit Cards Wisely

- Be Patient and Consistent

- Why a Good Credit Score Matters?

- Common Mistakes That Hurt Your Credit Score

- Team Final Thoughts

- FAQs

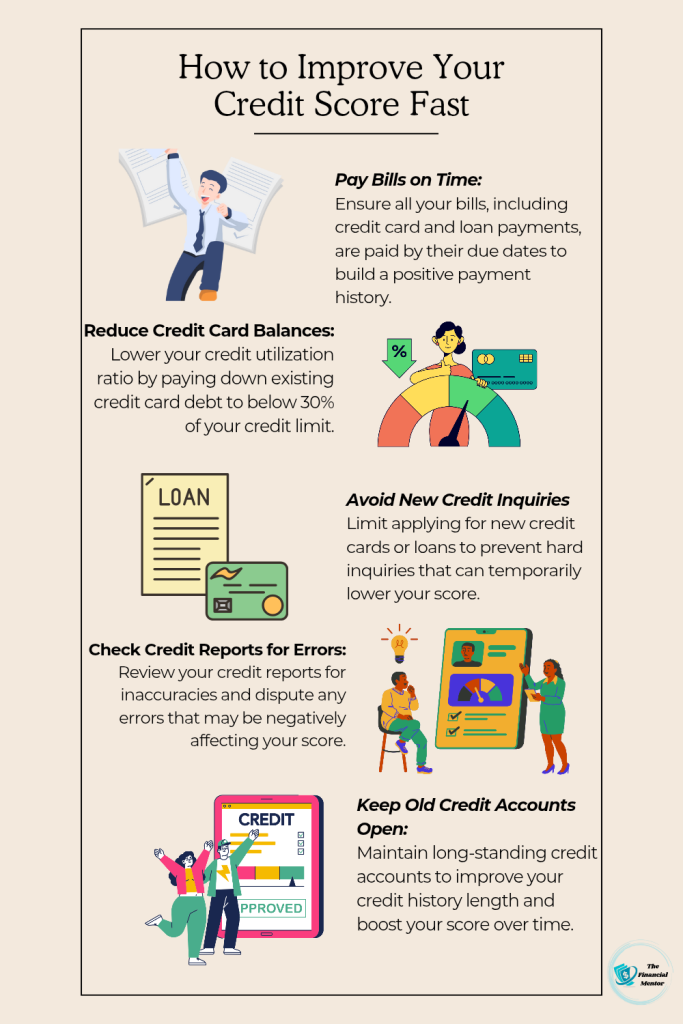

1. Pay Your Bills on Time

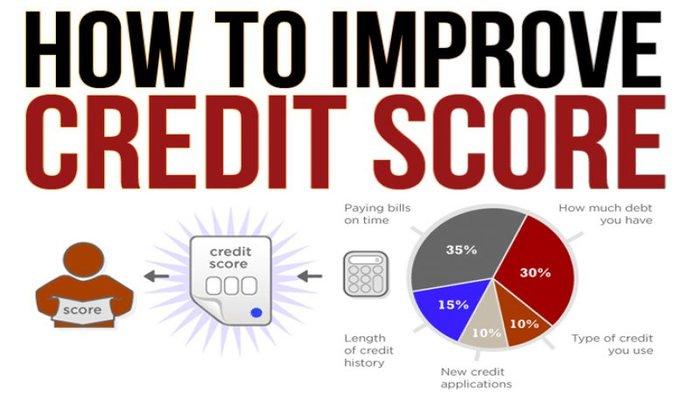

Payment history is one of the biggest factors affecting your credit score. Missing EMI payments, credit card bills, or loan installments can negatively impact your score.

To maintain a healthy credit score:

- Always pay your EMIs before the due date

- Set reminders or auto-pay options

- Avoid late payment penalties

Even a single missed payment can stay on your credit report for years. Consistent on-time payments show lenders that you are financially responsible.

2. Keep Your Credit Utilization Low

Credit utilization refers to the percentage of your credit limit that you use. Experts recommend keeping your utilization below 30%.

For example: If your credit card limit is ₹1,00,000, try not to use more than ₹30,000 regularly.

High credit utilization signals financial stress and can lower your score. To maintain low utilization:

- Avoid maxing out your credit cards

- Pay outstanding balances early

- Request a higher credit limit if necessary

Lower utilization improves your creditworthiness significantly.

3. Check Your Credit Report Regularly

Many people are unaware of errors in their credit reports. Incorrect information such as wrong loan details, duplicate accounts, or unauthorized transactions can hurt your score. You should check your credit report at least once every few months.

Look for:

- Incorrect personal information

- Unrecognized loans or credit cards

- Payment errors

- Duplicate entries

If you notice any mistake, immediately report it to the credit bureau for correction.

4. Avoid Applying for Multiple Loans Together

Every time you apply for a loan or credit card, lenders perform a hard inquiry on your credit report. Too many hard inquiries within a short period can reduce your score. Applying for multiple loans at once makes you appear credit-hungry to lenders.

Instead:

- Apply only when necessary

- Research eligibility before applying

- Space out your applications

Responsible borrowing behavior helps maintain a strong credit profile.

5. Maintain Old Credit Accounts

The length of your credit history also impacts your credit score. Older accounts show your long-term financial behavior and stability. Many people close old credit cards thinking it will help their score, but this can actually reduce it.

Benefits of keeping old accounts active:

- Longer credit history

- Better average account age

- Improved credit utilization ratio

Use old cards occasionally and keep them active by making small purchases and paying bills on time.

6. Diversify Your Credit Mix

Having a healthy mix of secured and unsecured loans can positively affect your credit score.

Examples include:

- Home loan

- Car loan

- Personal loan

- Credit cards

A balanced credit portfolio demonstrates that you can manage different types of credit responsibly. However, avoid taking unnecessary loans just to improve your credit mix. Borrow only when needed.

7. Clear Outstanding Debts Quickly

Outstanding debts and unpaid dues can significantly lower your credit score. If you have multiple debts, prioritize clearing high-interest loans first.

You can use strategies like:

- Debt snowball method

- Debt avalanche method

- Loan consolidation

Paying off debts improves your debt-to-income ratio and increases your financial credibility.

8. Avoid Settling Loans Improperly

Some people choose loan settlements when facing financial difficulties. While settlement may temporarily reduce your burden, it negatively affects your credit score. A “settled” status indicates that you did not fully repay the loan as agreed.

Instead of settlement:

- Negotiate better repayment terms

- Request EMI restructuring

- Discuss temporary relief options with lenders

A “closed” loan status is always better than “settled.”

9. Use Credit Cards Wisely

Credit cards can either improve or damage your credit score depending on how you use them.

Smart credit card habits include:

- Paying full bills every month

- Avoiding cash withdrawals

- Limiting unnecessary spending

- Using rewards responsibly

Never rely completely on minimum payments, as interest charges can accumulate quickly and increase debt. Responsible credit card usage builds trust with lenders and boosts your score over time.

10. Be Patient and Consistent

Improving a credit score does not happen overnight. It requires consistency, discipline, and responsible financial behaviour.

Focus on:

- Timely payments

- Low debt levels

- Controlled spending

- Regular credit monitoring

With time, your efforts will reflect positively in your credit report.

Why a Good Credit Score Matters?

A strong credit score offers several benefits, such as:

Easier Loan Approval

Banks and lenders prefer applicants with higher credit scores because they are considered low-risk borrowers.

Lower Interest Rates

A better score can help you secure loans at lower interest rates, saving money over time.

Higher Credit Limits

Financial institutions are more likely to offer higher limits to customers with good repayment history.

Better Financial Reputation

A healthy credit profile improves your overall financial credibility.

Common Mistakes That Hurt Your Credit Score

Avoid these common mistakes:

- Missing EMI payments

- Using full credit card limits

- Frequently applying for loans

- Ignoring credit report errors

- Defaulting on loans

- Closing old accounts unnecessarily

Being aware of these mistakes can help you protect your credit score effectively.

Team Final Thoughts : How to Improve Credit Score: 10 Effective Tips to Increase Your CIBIL Score

Your credit score is one of the most important indicators of your financial health. A good score can open doors to better financial opportunities, lower interest rates, and faster loan approvals.

The good news is that improving your credit score is completely achievable with proper planning and disciplined financial habits. Start by paying your bills on time, reducing debt, monitoring your credit report, and using credit responsibly.

Remember, small financial improvements today can create a stronger and more secure financial future tomorrow.

FAQs

A credit score above 750 is generally considered good by most lenders.

It may take a few months to a year depending on your financial behavior and repayment consistency.

No, checking your own credit score is considered a soft inquiry and does not affect your score.

Yes, timely repayment of loans and maintaining healthy financial habits can improve your score.

Yes, loan settlement can negatively affect your credit report and reduce your score.