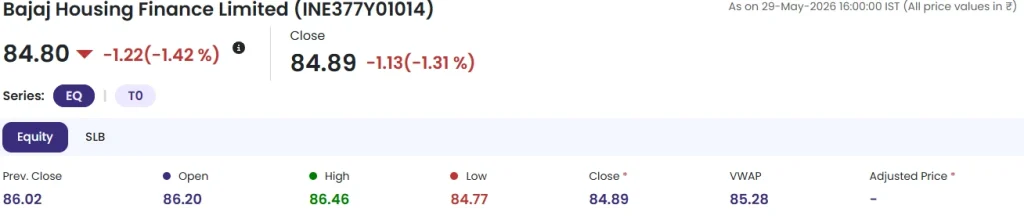

Bajaj Housing Share: Welcome in my Yono Informer website and here you will see full analysis report with company fundamental condition and future target. The issue price of Bajaj Housing Finance IPO was Rs.70, while its listing was at Rs 150 per share. This issue was subscribed 68 times.

A target of ₹850 for Bajaj Housing Finance is extremely determined from current levels and would require a combination of exceptional earnings growth, major valuation re-rating, and a very long investment horizon. Based on current fundamentals, ₹850 does not appear realistic in the near to medium term.

Table of Contents

- Business Strengths

- Why the Stock Has Struggled

- What Would Be Required for ₹850?

- Realistic Scenarios

- Conclusion

- My assessment

- FAQs

Business Strengths

Bajaj Housing Finance remains one of India’s fastest-growing housing finance companies. The company has consistently reported strong growth in Assets Under Management (AUM), profits, and loan disbursements while maintaining excellent asset quality.

Key positives include:

- FY26 AUM grew about 23% to over ₹1.4 lakh crore.

- FY26 profit after tax increased around 18% to ₹2,560 crore.

- Gross NPA remains very low at around 0.27%, reflecting strong underwriting standards.

- Q4 FY26 PAT rose 14% year-on-year, showing continued earnings momentum.

These are characteristics of a high-quality lender and justify a premium valuation compared with many housing finance peers.

Why the Stock Has Struggled

Despite strong fundamentals, the stock has underperformed since its euphoric post-IPO phase.

The main reasons include:

- Valuation correction – The stock was initially priced for perfection. As growth normalized, investors became less willing to pay extremely high multiples.

- Promoter stake sale concerns – Earlier block deals by the parent created supply pressure and raised fears of future stake dilution.

- Competition from banks – Large banks are aggressively targeting home loans, which could pressure margins over time. Brokerages have highlighted this risk despite remaining positive on the business.

What Would Be Required for ₹850?

Assume the stock trades around ₹90–100. A move to ₹850 would mean roughly an 8–9x increase in market value

For that to happen, the company would likely need:

- Sustained 20–25% earnings growth for many years.

- Return on Equity improving significantly.

- Continued leadership in housing finance.

- A premium valuation multiple maintained throughout the cycle.

- Favorable interest-rate and housing-market conditions

Even for a high-quality financial company, achieving an 8–9x return is a very demanding expectation.

Realistic Scenarios- Bajaj Housing Share

Bull case (5–10 years):

If Bajaj Housing Finance compounds earnings at 18–22% annually and maintains strong asset quality, a share price in the ₹250–450 range over the long term could be achievable. This would still represent excellent wealth creation.

Very bullish case:

If housing finance growth remains exceptionally strong and the company becomes the dominant private housing lender, prices above ₹500 could become possible over a longer horizon.

₹850 case:

This would require extraordinary execution and favorable market conditions over many years. It cannot be ruled out forever, but it should be viewed as an aggressive long-term aspiration rather than a reasonable near-term target.

Conclusion

Bajaj Housing Finance has strong fundamentals, high growth, low NPAs, and the backing of the Bajaj group. The business quality is not the issue. The challenge is valuation and the sheer scale of growth needed to justify ₹850.

My assessment: Bajaj Housing Share

Bajaj Housing Finance is a fundamentally strong company with healthy growth prospects, but ₹850 appears unrealistic in the near term given its current earnings and valuation. A gradual wealth-creation story is more likely than a rapid move to ₹850, unless the company delivers exceptional growth over many years.

- 1–3 years: ₹850 is highly unlikely.

- 5–7 years: Still difficult, though not impossible if growth remains exceptional.

- 10+ years: Possible only under a very strong bull-case scenario with sustained compounding.

Important Note:

We are not a financial advisor registered by SEBI, hence before investing in share market, please think once and invest as per your own risk. The stock market is full of risks in which your entire capital can become zero. You must consult your financial advisor before investing in the stock market.

FAQs

₹850 is possible only in a very optimistic long-term scenario. It would require sustained high earnings growth and a significant increase in valuation over many years.

Yes. The company has strong loan growth, low NPAs, healthy profitability, and backing from the Bajaj Finserv group.

Key risks include intense competition from banks, margin pressure due to interest-rate movements, and slower-than-expected growth in the housing finance sector.

Investors with a long-term horizon may find it attractive because of its growth potential, strong management, and expanding housing loan portfolio.

Strong earnings growth, increasing market share, improving return on equity, and favorable housing demand could support higher valuations over time.